RU

RU EN

EN CN

CN

Introduction: From Eco-Friendly Alternative to High-End Mainstream Technology

Over the past decade, UV curable inks have long been regarded as an eco-friendly alternative to solvent-based inks. Entering 2026, the industry positioning is undergoing a notable transformation. Tightening environmental regulations, the maturity of UV-LED curing technology, and the upgrading demand for packaging printing have driven UV inks to evolve from an "alternative technology" to a "high-end printing solution".

Especially in the fields of food packaging, label printing and flexible packaging, UV inks have become the preferred choice for an increasing number of printing enterprises by virtue of their fast curing speed, strong adhesion and low emission characteristics.

I. Market Size: Authoritative Data and Growth Forecast

The global UV curable ink market will maintain steady growth in 2026. Leading authoritative research institutions present different forecast ranges based on varied statistical scopes:

- Mordor Intelligence (January 2026): The global UV ink market size reached USD 1.75 billion in 2025, projected to reach USD 1.88 billion in 2026 and USD 2.65 billion by 2031, with a compound annual growth rate (CAGR) of 7.17% from 2026 to 2031.

- 360 Research Reports (March 2026): The global UV ink market size is estimated at USD 4.227–4.550 billion in 2026, expected to grow to USD 13.814–14.074 billion by 2035, representing a CAGR of 13.13%–14.3% from 2026 to 2035.

- Global Environmental Protection Research Network (GEP Research, January 2026): The global UV ink market size is forecasted at approximately USD 6.2 billion in 2026, and is expected to exceed USD 8 billion by 2030.

Explanation of Data Differences: The discrepancies among institutional data stem from different statistical coverage. Mordor Intelligence focuses exclusively on printing-grade UV inks, while 360 Research, GEP Research and other agencies cover full-range UV curing materials including industrial coating, electronics and automotive sectors. Synthesizing mainstream institutional data, the core market size range of global UV inks in 2026 is USD 4.2–6.2 billion, and the medium-to-long-term CAGR (2026-2033) is concentrated at 7%–14%. Environmental policies and downstream industry demand act as the core driving forces for market growth.

II. Core Driving Factors

(1) Tightening Environmental Policies Boost Surging Demand for Low-VOC Products

Under the global carbon peaking and carbon neutrality goals, regulations including EU REACH, U.S. EPA standards and China GB 38507-2020 have continuously tightened VOC emission limits. UV inks feature nearly zero VOC emissions, showing significant advantages over solvent-based inks with VOC content of 30%–70%, making them the compliant preferred option for high-end packaging and printing industries. From 2024 to 2025, the global patent applications for low-migration and low-odor photoinitiators increased by 40% year-on-year, directly driving the penetration growth of UV inks in food contact material applications.

(2) Booming Downstream Demand Led by the Packaging Industry

- Packaging Industry (accounting for over 45%): Surging demand for inks with high adhesion, friction resistance and low migration in food, beverage, pharmaceutical and daily chemical sectors. For instance, beverage brands adopt UV printing on metal bottle caps to adapt to cold chain environments; UV inks used in pharmaceutical packaging comply with ISO 10993 biocompatibility standards.

- Electronics Industry: UV inks are suitable for printing on heat-sensitive substrates such as PCB, touch panels and anti-glare coatings of display screens. A leading smartphone manufacturer reduced the defective rate of display coatings by 30% after switching to UV inks.

- Automotive Industry: UV curable inks are widely applied to automotive interior parts (instrument panels, control buttons) and exterior decorative films, offering both weather resistance and decorative performance.

- Digital Printing: Growing demand for personalized packaging and short-run order printing. UV inkjet inks have become core materials for digital printing due to their high resolution and instant curing properties.

(3) Technological Upgrading: LED-UV Becomes Mainstream

- LED-UV curing technology reduces energy consumption by 60%–65% compared with traditional mercury lamps, featuring mercury-free pollution and a 5-fold longer service life of equipment. The global penetration rate of LED-UV inks reached 35% in 2025, and is projected to surpass 50% by 2028.

- Low-migration photoinitiators: Targeting restricted substances such as ITX and BP, new-type photoinitiators (e.g., acylphosphine oxides) have gained rapidly rising market share, accounting for 40% of the market in 2025.

III. Market Segmentation Pattern

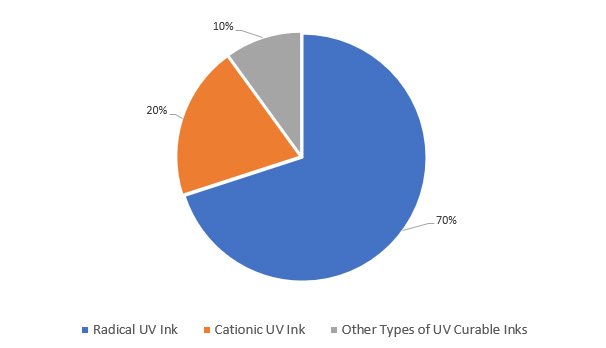

(1) Product Type Structure (2026)

- Free Radical UV Inks (about 70% market share): Fast curing speed and low cost, dominating packaging and commercial printing fields.

- Cationic UV Inks (about 20% market share): Superior adhesion and low shrinkage rate, suitable for difficult-to-adhere substrates such as glass and metal.

- Other Types of UV Inks (about 10% market share): Including bio-based UV inks, photo-induced radical/cationic hybrid systems and other categories.

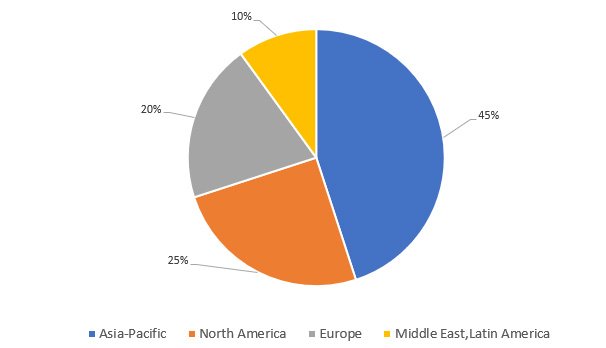

(2) Regional Market Distribution (2026)

- Asia-Pacific Region (about 45% market share): China, India and Southeast Asia serve as the core growth engines. China’s UV ink market size is expected to reach USD 1.8–2.2 billion in 2026, accounting for around 35% of the global total, ranking as the world’s largest producer and consumer market.

- North America (about 25% market share): Dominated by the United States with stringent environmental regulations. The penetration rate of LED-UV and low-migration inks exceeds 40%, leading the global industry.

- Europe (about 20% market share): Germany and Italy are core regional markets. The EU REACH regulation promotes the R&D and application of bio-based UV inks, with the proportion of bio-based raw materials reaching 15% in 2025.

- Latin America, Middle East & Africa (about 10% market share): Maintaining a rapid growth rate with a CAGR of approximately 9%, driven mainly by demand from packaging and label printing industries.

(3) Competitive Landscape (2026)

The global UV ink market features high concentration with leading enterprises dominating the industry:

- DIC (Japan): Holding around 18% market share, as the global industry leader with full-category technology layout and prominent advantages in the packaging sector.

- Flint Group (Finland) / Siegwerk (Germany): Each capturing 12%–15% market share, leading European suppliers with strong competitiveness in high-end packaging and commercial printing markets.

- Toyo Ink (Japan), Fujifilm (Japan): Each occupying 8%–10% market share, holding technological leadership in electronics and digital printing fields.

- Chinese Enterprises (e.g., StarColor): Capturing a combined market share of about 15%, focusing on the mid-to-low-end market and gradually making breakthroughs in high-end LED-UV and premium UV ink sectors.

IV. Industry Development Trends

(1) Eco-Friendliness: Bio-Based and Low-Migration Become Industry Standards

- Bio-based UV Inks: Adopting renewable raw materials such as soybean oil and castor oil to replace petroleum-based resins. The proportion of bio-based raw materials is expected to reach 30% by 2030.

- Photoinitiator-Free System: Electron Beam (EB) curing technology is gradually commercialized, completely eliminating the migration risk of photoinitiators, with an estimated CAGR of 20% from 2026 to 2033.

(2) Technological Integration: Acceleration of Digitalization and Intellectualization

- UV + Digital Printing: Rising demand for on-demand printing and variable data printing. UV inkjet inks are compatible with high-speed digital printing presses, and the related market size is expected to reach USD 1.5 billion by 2030.

- Smart Inks: UV curable color-changing, conductive and antibacterial inks are gradually applied to smart packaging and flexible electronics. The annual growth rate of relevant patent applications maintained at 50% from 2025 to 2030.

(3) Market Differentiation: Parallel Development of High-End Upgrade and Localization

- High-End Market: Surging demand for low-migration, high-stability and functional inks in food contact, medical and electronic fields. Leading enterprises maintain high gross profit margins through technological barriers.

- Mid-to-Low-End Market: The rise of local enterprises in emerging markets such as China and India seizes market share with cost advantages and rationalizes the global price system.

(4) Supply Chain Restructuring: Regionalization and Security

- Against the backdrop of global trade frictions and post-pandemic industrial adjustment, European and American enterprises have accelerated nearshoring outsourcing, making the Asia-Pacific region (China, Vietnam, Malaysia) the core production base.

- The supply chain of core raw materials such as photoinitiators and resins has become diversified to reduce reliance on single suppliers. The global self-sufficiency rate of core raw materials reached 85% in 2025.

Data Source Disclaimer

The core data of this report are sourced from authoritative industry reports released between January and May 2026, including:

- Mordor Intelligence UV Cured Printing Inks Market Size & Share Analysis (2026-2031);

- 360 Research Reports UV (Ultraviolet) Curable Inks Market Size, Share, Growth, and Industry Analysis (2026-2035);

- Global Environmental Protection Research Network (GEP Research) Global UV (Ultraviolet Curable) Ink Market Report (2026);

- Market Research Intellect UV Curable Ink Market By Product (2026-2033).